ReSource is a Mutual Credit protocol that allows participants to access credit at extremely competitive terms, often at 0% interest, while freeing them from their dependence on external capital providers such as banks, creditors, or even investors.

Arguably, to many this may sound too good to be true. Afterall, who in their right mind would lend money to anyone without charging interest or while settling for minor fees that are easily outcompeted by better investment opportunities? To answer this question we first need to understand what Mutual Credit is, what its shortcomings are, and how ReSource uses blockchain technology to overcome them.

What is Mutual Credit

First of all, let us clear some confusing terminology. Mutual Credit shouldn’t be confused with Mutual Banking, Credit Unions, or Cooperative Banking. While Mutual Credit shares similar ideological roots with the now widely proliferated concept of Cooperative Banking, the two terms refer to two different institutions. While a Credit Union is just a normal bank that happens to be owned by its customers, sharing profits with them and offering them fairer terms on their loans, Mutual Credit is a much farther reaching concept, attempting to fundamentally change what credit actually is.

While a Credit Union depends on the aggregated capital of its members, which it then manages, loans out and invests on their behalf, a Mutual Credit system is not dependent on pre-existing capital in the form of money, but rather relies on the non-monetary resources of its members (such as unsold inventory, productive capacities etc), to create its own internal commodity-backed monetary system.

Being able to create their own money, Mutual Credit systems are freed from the need to “rent” money from a creditor (or cooperative members) in order to lend it out to third parties. This trick is what allows Mutual Credit to be available at close to 0% interest.

“Creating your own money” may sound dangerous; or even shady, but it’s far from it. In contrast to the fiat money we’re used to, or even new forms of blockchain-based currencies such as Bitcoin, Mutual Credit money is more of an accounting device that keeps track of mutual obligations. It is, if you will, a physical (or digital) representation of a ledger entry, that by its very nature tends to preserve its value. Let us explain:

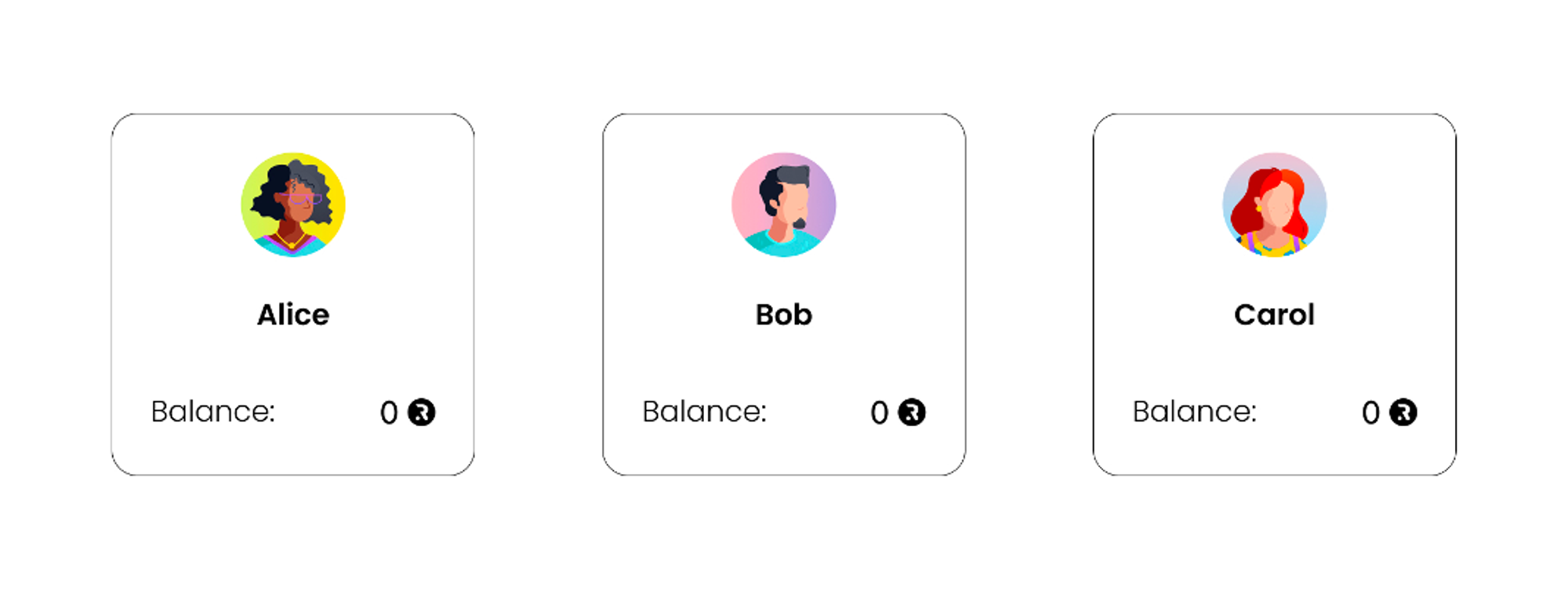

The example below depicts a simple Mutual Credit system with only three members: Alice, Bob, and Carol. The three of them don’t have any money, but they do have productive capacities. All three of them are able to deliver goods or provide services — if not now, then at some point in the foreseeable future.

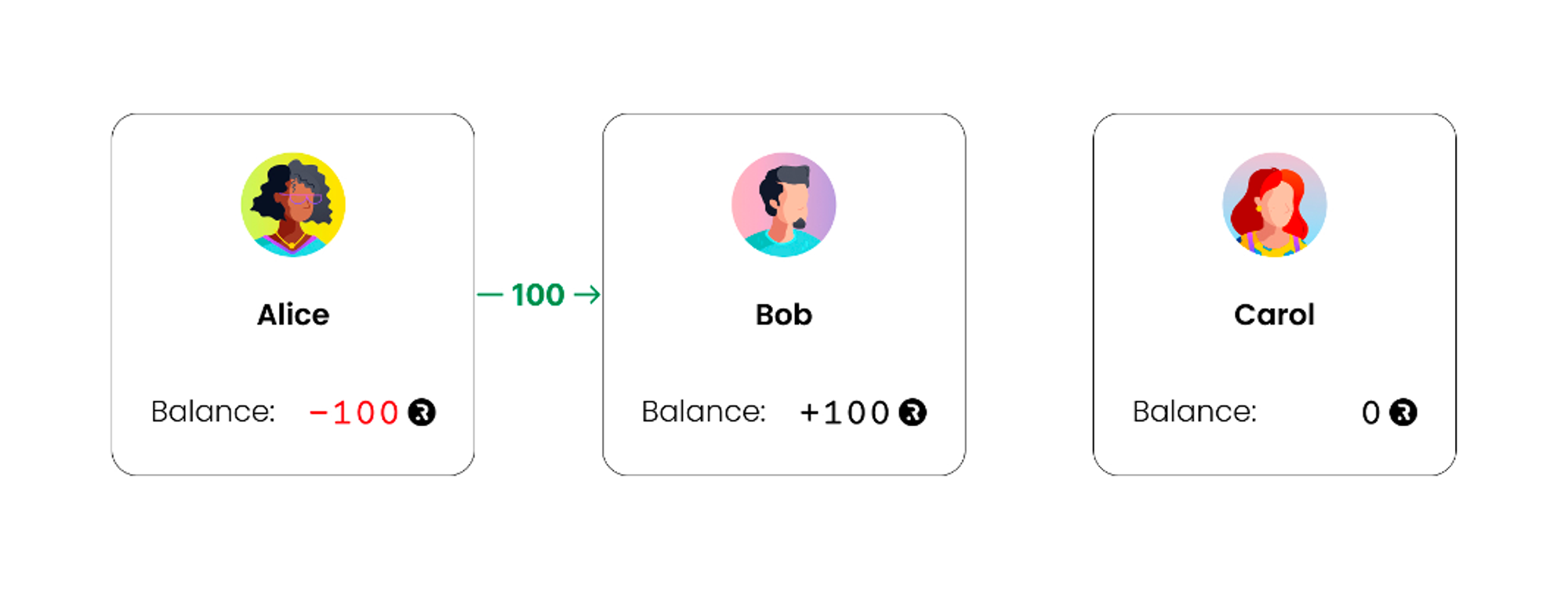

Money is introduced into the system once a participant, Alice, decides to purchase an item from another participant, Bob. When she does so, a deficit is created on her account and a deposit appears on Bob’s account. This way money is effectively “spent into existence”.

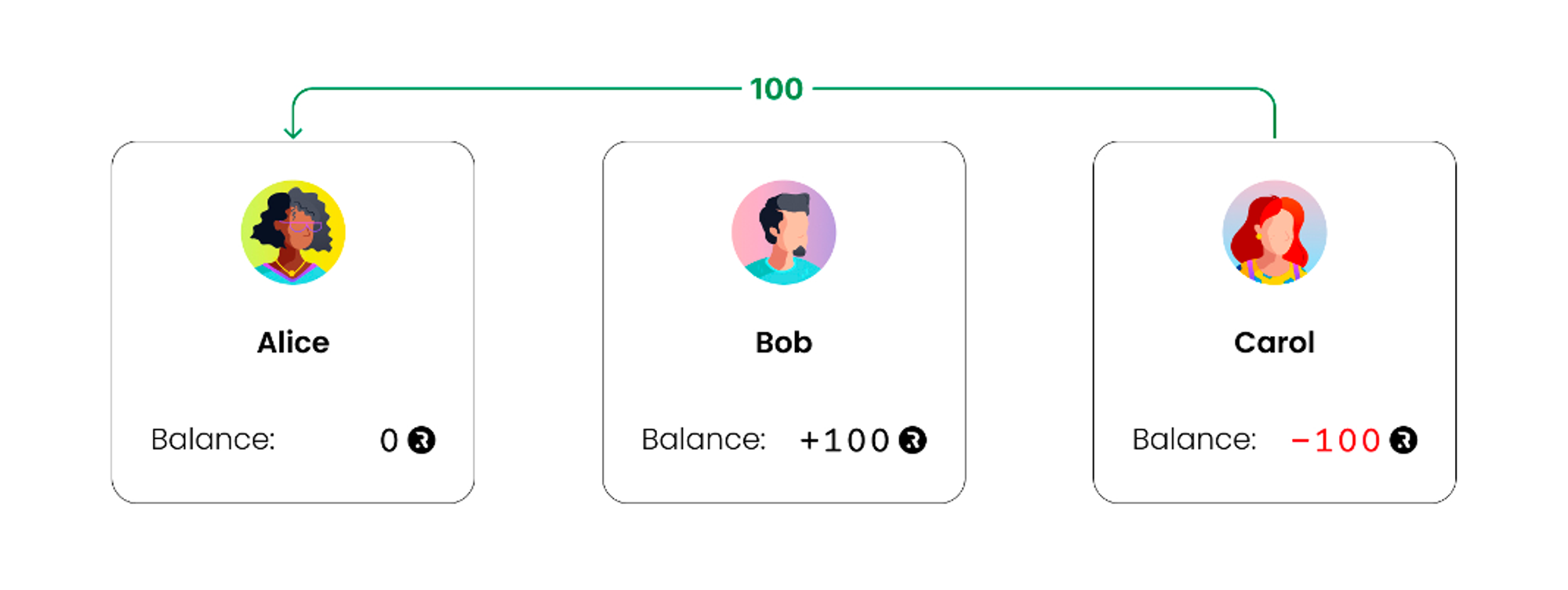

In the same way, Carol overdrafts her account in order to purchase an item or service from Alice. This returns Alice’s balance to zero.

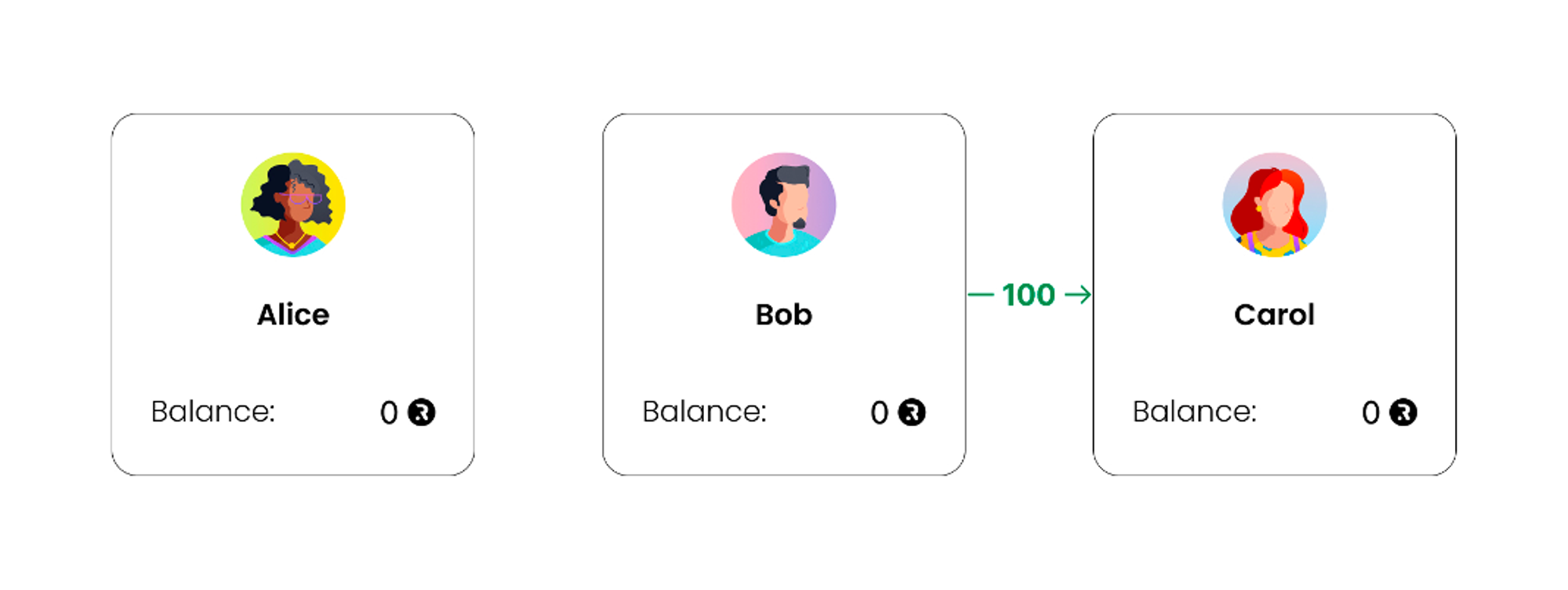

If Bob now decides to purchase an item or service from Carol, his deposits will be remitted to her, covering Carol’s deficit while returning both of their balances to zero. At this stage, the network will return to its equilibrium zero-deposit state in which no debt, and hence no money, exists within the system.

You may have already spotted an important attribute of Mutual Credit systems: The amount of money within it equals the amount of debt, or obligations among its members. This is where Mutual Credit money derives its intrinsic value from: each money unit in existence is required by someone within the system to pay their debts. This means that the existing money supply always matches the demand exercise on it by outstanding loans. In later posts we will come back to this point and elaborate on it further, but let us recognise for now that as long as the system can deal with defaults, monetary stability is fundamentally guaranteed.

As a three player game, this system is obviously very limited in scope and utility. For this to make sense, we need to presuppose that Alice, Bob and Carol are able to match each other’s demand with the supply they are able to generate. However, not dissimilar from Social Networks, the ability of the network to match demand with supply grows exponentially with its size. A trading network consisting of hundreds of members can already facilitate meaningful trade, the moment we get into the thousands we have a functioning micro-economy.

Where’s the Catch?

Ok, so if it is that easy to create your own micro economy in which liquidity is always available — when and where it is required — then why didn’t this concept outcompete the often exploitative credit practices commonplace in traditional finance?

Well, with all its obvious benefits, Mutual Credit comes with a few drawbacks that have so far complicated its growth and adoption. Addressing these shortcomings is the whole raison d’etre of the ReSource project. What these shortcomings are and how we at ReSource use DLT and DeFi mechanisms to address them will be discussed in our upcoming post.

See you there!

In the meantime, if you have questions and want to learn more about Mutual Credit and ReSource, join us on Discord and Telegram, and follow us on Twitter.

Your Friends at ReSource.